The Freight Economist

Weekly market update

The Freight Economist is back -- now every week -- to deliver the data-driven market intelligence your business needs to stay ahead. Read on for an essential breakdown of June’s soaring freight rates, shifting driver employment numbers, and our short-term outlook to help you prepare your capacity for the fall.

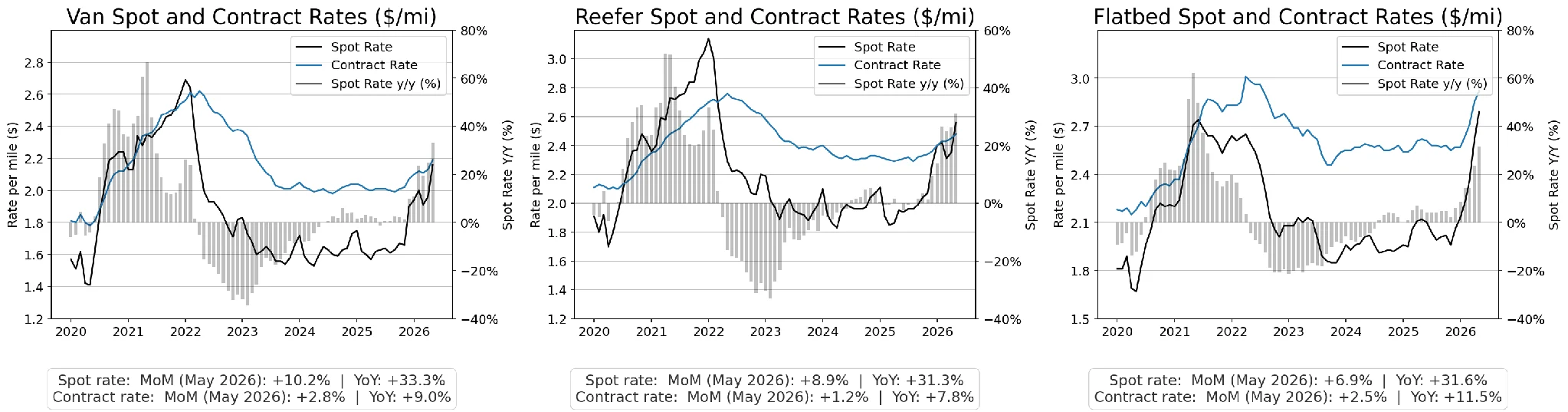

Produce volumes propelled the spot market in June

The national average dry van spot rate exceeded $3/mi for the first time since March 2022.

Spot rates surged:

Van: 45% y/y excluding fuel

Reefer: 39% y/y

Flatbed: 40% y/y

Contract rates followed

Contract rates rose across all trailer types (10% to 18% y/y).

Diesel prices fell

The average diesel price per gallon fell 10% m/m.

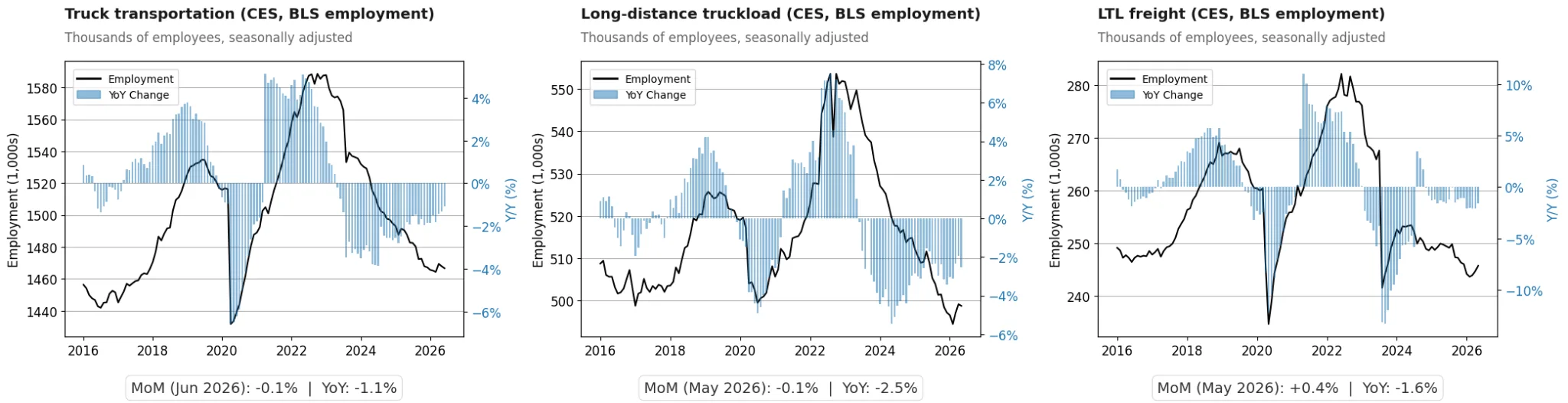

Trucking employment fell in June despite the tightening market

Trucking employment typically lags spot rates by a few months; as rates rise, carriers generally accelerate hiring. Currently, however, carriers are navigating a strict regulatory landscape. Trucking employment fell 0.1% month-over-month in June and was down 1.1% year-over-year. In the long-distance truckload sector specifically, employment was 2.5% lower year-over-year as of May. If employment fails to recover, the current market tightness could be prolonged.

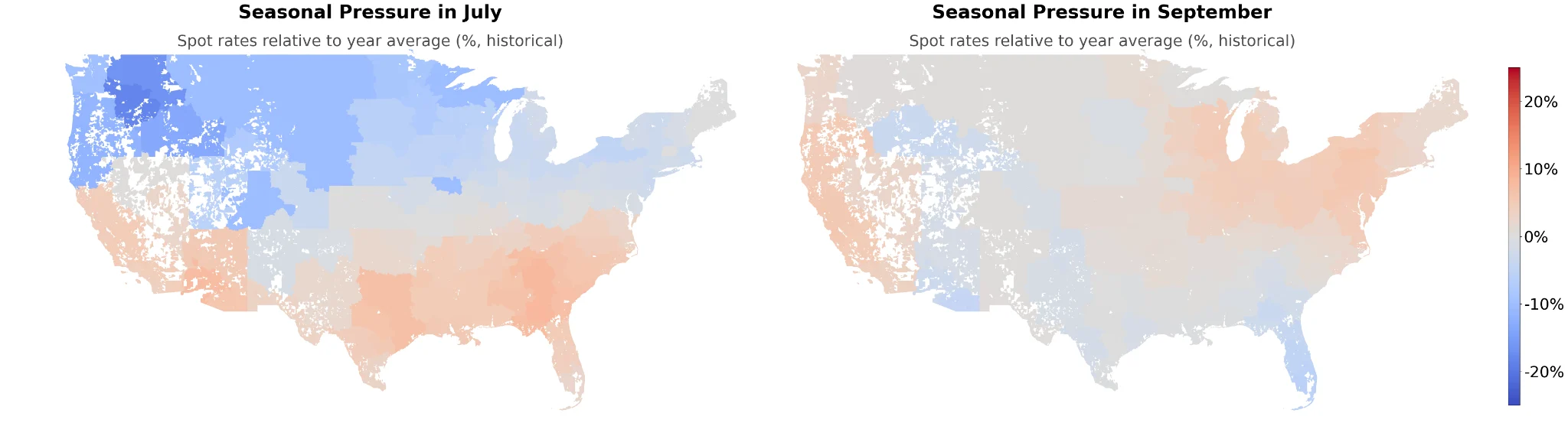

Short-term market outlook: Summer and peak season

Following the 4th of July, the market typically enters a period of stabilization as demand cools between the summer produce rush and the Q4 peak season. Some Southern markets are expected to remain tight in July. In addition, as the weeks progress, capacity will begin to tighten in Western and Northern regions, particularly around port hubs, as shippers prepare for the upcoming peak season. If nationwide tightness persists in August and September, prepare for a tighter peak season in Q4.